Investing in stocks always involves risk. One of the most severe outcomes is when a company’s stock becomes nearly worthless. This is often referred to as a stock “going to zero.” However, the phrase can be misleading. A company’s shares rarely drop to an exact price of $0.00, and not every bankruptcy ends in a total loss for shareholders. In fact, the reality is more complex and often misunderstood.

This article explains what it really means when a stock “goes to zero,” how it can happen, why it doesn’t always mean a complete loss, and how investors can protect themselves from this kind of risk.

Understanding What It Means for a Stock to “Go to Zero”

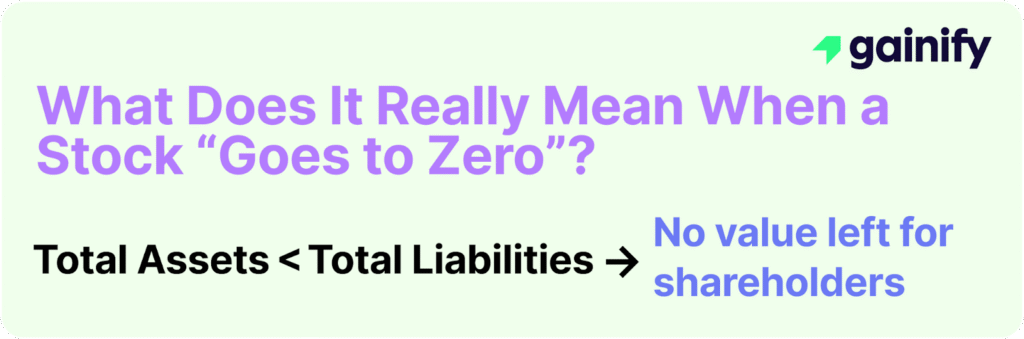

When people say a stock has “gone to zero,” they usually mean that its value has fallen so much that the market believes the company’s shares are no longer worth anything. This does not always mean the share price is exactly $0.00 — in fact, the stock might still be trading for a few cents. But the key idea is that investors no longer expect any meaningful recovery or future value from the company.

This situation typically arises when a company is under severe financial stress — for instance, it may be facing a significant liquidity shortfall, struggling to refinance debt, or experiencing sustained operating losses. In such cases, the company may be on the verge of bankruptcy, entering a formal restructuring process, or preparing for asset liquidation.

However, for shares to become truly worthless, the company’s liabilities must exceed the fair market value of its assets, leaving no residual value for common shareholders after all creditors and other obligations are paid. This condition is most often confirmed during liquidation under bankruptcy proceedings, where the capital structure is fully consumed by debt and senior claims.

In short a Stock Goes to Zero when:

Once all the company’s assets are sold off, the money goes to pay banks, bondholders, and other creditors first. Shareholders are last in line. If there is nothing left after the debts are paid, the shares have no value. That is what “going to zero” really means: the company has no leftover value for the people who own its stock.

Why Do Some Stocks Still Trade After Bankruptcy?

After filing for bankruptcy, many companies are delisted from major exchanges but continue to trade on over-the-counter (OTC) markets. These post-bankruptcy shares often trade at fractions of a cent, not because they retain real underlying value, but because speculative investors are betting on a possible recovery, legal settlement, or restructuring windfall.

In reality, these securities are highly risky, detached from fundamentals, and often reflect false hope rather than true economic worth. In most cases, they are eventually cancelled or become untradeable once the bankruptcy process concludes and common equity is extinguished.

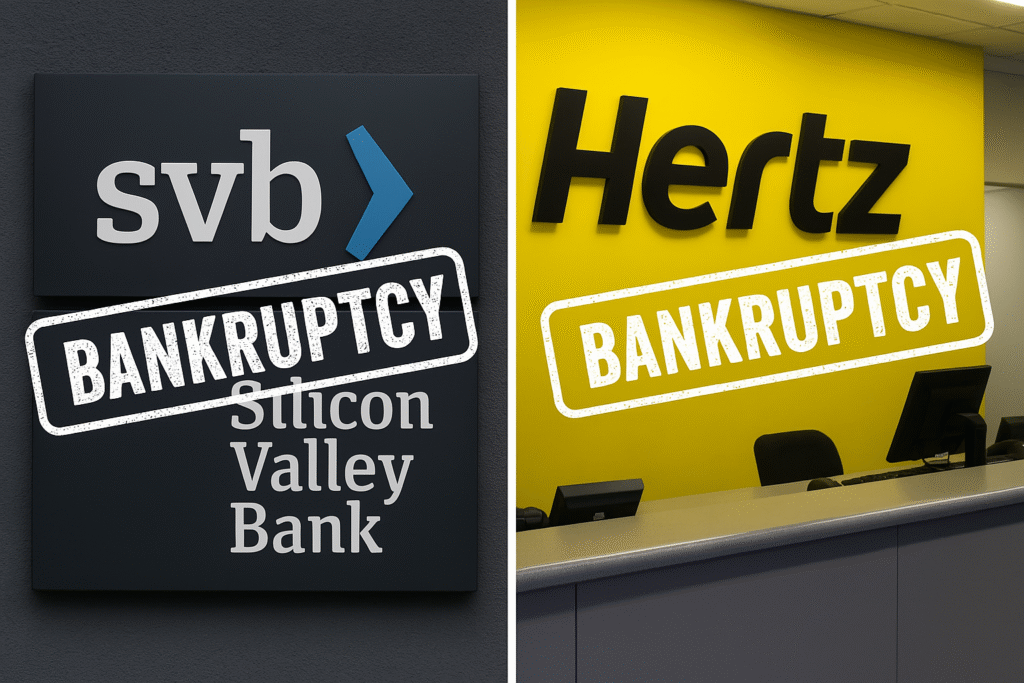

Case Study 1: Silicon Valley Bank (2023)

Outcome: Near-total equity loss with low probability of recovery

In March 2023, Silicon Valley Bank (SVB), a key financial partner to the tech and venture capital sectors, collapsed after a rapid run on deposits exposed severe liquidity mismatches in its balance sheet. The bank’s long-dated bond portfolio, impaired by rising interest rates, forced a fire sale of assets at significant losses.

SVB Financial Group, the bank’s parent company, filed for Chapter 11 bankruptcy shortly after the FDIC seized the bank. While the stock was delisted from the NASDAQ, shares continued to trade over-the-counter at a few cents per share, driven by speculative interest.

However, the financial reality was stark. The parent company held limited assets, most of which were pledged or inaccessible, and faced substantial legal liabilities. Analysts widely viewed any shareholder recovery as highly unlikely. As of early 2025, no material recovery has occurred, and common equity is expected to be fully extinguished.

Key Lesson: Just because a stock trades post-bankruptcy does not mean it holds value. In SVB’s case, the trading price reflected speculative activity, not any meaningful likelihood of recovery.

Case Study 2: Hertz Global Holdings (2020–2021)

Outcome: Partial equity recovery following unexpected turnaround

Hertz filed for Chapter 11 bankruptcy in May 2020 after a collapse in global travel demand during the COVID-19 pandemic devastated its rental car business. Initially, the stock was expected to be wiped out, and many observers assumed shareholders would be left with nothing.

Surprisingly, retail traders continued to buy the stock aggressively on the OTC market, believing in a potential recovery. That speculation became partially validated when, in 2021, a consortium of investors led by Knighthead Capital and Certares Management won a bidding process to take the company out of bankruptcy. As part of the reorganization plan, existing shareholders received a combination of cash, new equity, and warrants.

Common shareholders ultimately recovered over $7 per share — an extremely rare outcome in a Chapter 11 case.

Key Lesson: While Hertz was an exception, it shows that equity recovery is possible in bankruptcy when underlying assets retain value and market conditions shift. However, this is the outlier, not the norm.

Why Are Shareholders Last in Line?

In a corporate capital structure, each stakeholder group has a specific legal claim on the company’s assets. When a company becomes insolvent or enters bankruptcy, these claims are settled in a strict order of priority during the liquidation or restructuring process.

- Secured creditors – These are lenders whose loans are backed by collateral, such as banks holding claims on physical assets.

- Unsecured creditors – This group includes bondholders, suppliers, and other parties without collateral protection.

- Preferred shareholders – Investors who hold preferred equity are next, with priority over common shares but still subordinate to all debt.

- Common shareholders – Owners of ordinary shares are last in line and are only entitled to residual value, if any remains.

If the value of the company’s assets is insufficient to fully repay debts and senior claims, there is nothing left for common shareholders. This is why, in most bankruptcy scenarios, common equity loses nearly all its value. The economic rights tied to future earnings or liquidation proceeds are effectively eliminated.

How Investors Can Mitigate the Risk of Total Equity Loss

While complete equity losses are relatively uncommon, particularly among large and well-established companies, they remain a real risk. Investors can reduce their exposure to these extreme outcomes by applying a disciplined, risk-aware approach:

- Maintain diversification across sectors, geographies, and market capitalisations to avoid concentrated exposure to any single company or industry downturn.

- Assess balance sheet strength, focusing on debt levels, liquidity, interest coverage, and refinancing risk.

- Monitor early warning signals, including missed debt payments, changes in auditor status, delayed filings, executive resignations, or covenant breaches.

- Limit exposure to speculative or distressed equities, especially those with weak fundamentals or unclear paths to profitability.

Ultimately, companies with solid balance sheets, predictable cash flows, and well-managed capital structures are far more likely to preserve shareholder value through periods of volatility or financial stress.

Final Perspective: A Stock Hitting Zero Is Rare, but Not Impossible

A stock becoming completely worthless is a rare but serious outcome. It typically occurs when a company is overwhelmed by debt, suffers from poor financial management, or is unable to recover from a major operational or market disruption.

It is important to understand that bankruptcy does not automatically result in a total loss for shareholders. In some cases, companies restructure successfully and shareholders may receive some form of recovery. However, when a company’s liabilities significantly exceed the value of its assets, the legal and financial structure leaves no room for common equity to retain value.

Avoiding these situations requires more than intuition. It calls for detailed financial analysis, a thoughtful approach to diversification, and consistent risk management. Investors who understand how capital structures work, remain vigilant for early signs of distress, and act decisively are far more likely to protect their capital over time.

5. The Psychology of Money by Morgan Housel

Best for: Building the right mindset and understanding the behavioral side of investing

Level: Beginner

Focus areas: Financial behavior, emotion, risk perception, habits

Overview:

This book offers a fresh perspective: success in investing has less to do with intelligence and more to do with behavior. Housel blends storytelling with practical insights on how people think about money, risk, and wealth over time.

Why it matters for beginners:

It’s one of the most approachable books on finance. Readers learn that managing money well often means managing oneself — expectations, patience, and emotional reactions.

Top Quote (Exact):

“Doing well with money has little to do with how smart you are and a lot to do with how you behave.”

Final Thoughts: The Best Investing Education Starts with Timeless Wisdom

These five books provide an exceptional foundation for anyone new to investing. Each one tackles a different, critical piece of the puzzle — from understanding the market to managing behavior, from building a portfolio to choosing the right strategy. More importantly, they teach patience, discipline, and clarity — the very traits that separate successful investors from short-term speculators.

If you are just getting started, any one of these books will give you tools and insight that will serve you for decades. If you read all five, you will not just be better informed — you will be far better equipped to grow and protect your financial future.